Telecom & Allied Sector 2022

Indian Economy:-

- India has emerged as the fastest growing major economy in the world and is expected to be one of the top three economic powers in the world over the next 10-15 years, backed by its robust democracy and strong partnerships.

- India’s nominal gross domestic product (GDP) at current prices is estimated to be at Rs. 232.15 trillion (US$ 3.12 trillion) in FY22.

- Minister of Commerce and Industry, Consumer Affairs, Food and Public Distribution and Textiles Mr. Piyush Goyal said that India will achieve exports worth US$ 1 trillion by 2030. India's electronic exports are expected to reach US$ 300 billion by 2025-26. This will be nearly 40 times the FY2021-22 exports (till December 2021) of US$ 67 billion.

- India is expected to be the third largest consumer economy as its consumption may triple to US$ 4 trillion by 2025, owing to shift in consumer behaviour and expenditure pattern, according to a Boston Consulting Group (BCG) report. It is estimated to surpass USA to become the second largest economy in terms of purchasing power parity (PPP) by 2040.

- The war in Ukraine has triggered a costly humanitarian crisis that, without a swift and peaceful resolution, could become overwhelming. Global growth is expected to slow significantly in 2022, largely as a consequence of the war.

- The economic costs of war are expected to spread farther afield through commodity markets, trade, and—to a lesser extent—financial interlinkages. Fuel and food price rises are already having a global impact, with vulnerable populations—particularly in low-income countries—most affected. As a result, interest rates had risen sharply and asset price volatility had increased since the start of 2022—hitting household and corporate balance sheets, consumption, and investment.

Telecom Industry in India:-

- Currently, India is the world’s second-largest telecommunications market with a subscriber base of 1.16 billion and has registered strong growth in the last decade. In 2019, India surpassed the US to become the second largest market in terms of number of app downloads.

- The Government has enabled easy market access to telecom equipment and a fair and proactive regulatory framework, that has ensured availability of telecom services to consumer at affordable prices. The deregulation of Foreign Direct Investment (FDI) norms have made the sector one of the fastest growing and the top five employment opportunity generator in the country.

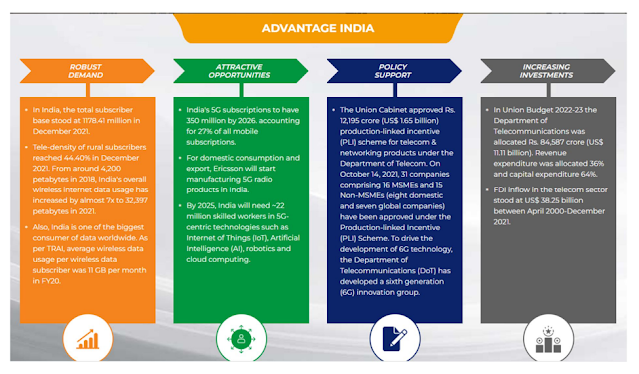

- India is the world’s second-largest telecommunications market. The total subscriber base, wireless subscriptions as well as wired broadband subscriptions have grown consistently. Tele-density stood at 85.91%, as of December 2021, total broadband subscriptions grew to 792.1 million until December 2021 and total subscriber base stood at 1.18 billion in December 2021.

- Gross revenue of the telecom sector stood at Rs. 64,801 crore (US$ 8.74 billion) in the first quarter of FY22.

- The total wireless data usage in India grew 16.54% quarterly to reach 32,397 PB(Petabytes) in the first quarter of FY22. The contribution of 3G and 4G data usage to the total volume of wireless data usage was 1.78% and 97.74%, respectively, in the third quarter of FY21. Share of 2G data usage stood at 0.48% in the same quarter.

- Over the next five years, rise in mobile-phone penetration and decline in data costs will add 500 million new internet users in India, creating opportunities for new businesses.

- By 2025, India will need ~22 million skilled workers in 5G-centric technologies such as Internet of Things (IoT), Artificial Intelligence (AI), robotics and cloud computing.

Investment & Major developments in the sector:-

- FDI inflow in the telecom sector stood at US$ 38.25 billion between April 2000-December 2021.

- In January 2022, Google made a US$ 1 billion investment in Airtel through the India Digitization Fund.

- In October 2021, Vodafone Idea stated that it is in advanced talks to sell a minority stake to global private equity investors including Apollo Global Management and Carlyle to raise up to Rs. 7,540 crore (US$ 1 billion) over the next 2-3 months.

- In October 2021, British satellite operator Inmarsat Holdings Ltd. announced that it is the first foreign operator to get India’s approval to sell high-speed broadband to planes and shipping vessels. Inmarsat will access the market via Bharat Sanchar Nigam Ltd. (BSNL) after BSNL received a license from the Department of Telecommunications.

- In October 2021, Dixon Technologies announced plans to invest Rs. 200 crore (US$ 26.69 million) under the telecom PLI scheme; this investment will include the acquisition cost of Bharti Group’s manufacturing unit.

- In September 2021, Bharti Airtel announced an investment of Rs. 50 billion (US$ 673 million) in expanding its data centre business to meet the customer demand in and around India.

- In August 2021, Tata Group company Nelco announced that the company is in talks with Canadian firm Telesat to sign a commercial pact for launching fast satellite broadband services in India under the latter’s Lightspeed brand, a move which will pit the combined entity against Bharti Enterprises-backed OneWeb, Elon Musk’s SpaceX and Amazon.

- In March 2021, Vodafone Idea Ltd. (VIL) announced that the acquired spectrum in five circles would help improve 4G coverage and bandwidth, allowing it to offer ‘superior digital experience’ to customers.

- In March 2021, Advanced Television Systems Committee (ATSC) and Telecommunications Standards Development Society, India (TSDSI) signed a deal to boost adoption of ATSC standards in India in order to make broadcast services available on mobile devices. This allows the TSDSI to follow ATSC standards, fostering global digital broadcasting standard harmonisation.

- In the first quarter of FY21, customer spending on telecom services increased 16.6% y-o-y, with over three-fourths spent on data services. This spike in consumer spending came despite of the COVID-19 disruption and lack of access of offline recharges for a few weeks

- India had over 500 million active internet users (accessed Internet in the last one month) as of May 2020.

- According to a Zenith Media survey, India is expected to become the fastest-growing telecom advertisement market, with an annual growth rate of 11% between 2020 and 2023.

- The Indian Government is planning to develop 100 smart city projects, and IoT will play a vital role in developing these cities. The National Digital Communications Policy 2018 envisaged attracting investment worth US$ 100 billion in the telecommunications sector by 2022. App downloads in India is expected to increase to 37.21 billion in 2022F.

Edge data center and its Future:-

- As digital transformation sweeps across our society and economy, expansion of internet infrastructure must follow the data and with the anticipation of 5G mobile networking connectivity means networks want to get closer to the edge where edge computing will capture, process, analyse data at the edges (Fulton III, 2020). This decentralised approach, brings the data closest to the point of interaction, and takes place in what we now call edge data center. In understanding the ecosystem of edge computing and edge data center, one has to grasp the basic knowledge from the beginning.

What is edge computing?

- Edge computing, one of the most recent buzzword in tech, can be challenging to understand as data processing can happen in many ways and in different settings. It is the science of capturing, processing, and analysing data near to its creation point. This is done without having the need for the data to be transported to another server environment in a centralized data center but instead processed locally and possibly real time in the edge data center (Overby, 2019), highlighting its main difference between cloud computing architecture. The main concept is to bring computing services closer to data sources or local end users.

- In other words, Edge computing is a family of technologies that distributes application data and services where they can best optimize outcomes in a growing set of connected assets. It includes edge infrastructure and edge analytics software.

- When talking about reaping the benefits of digital transformation, the full potential cannot be appreciated if it only depends on cloud computing due to its latency as it is no longer cutting when it comes to deploying artificial intelligence machine and getting real-time results. In short, it solves the key challenges of bandwidth, latency, resiliency, and data sovereignty.

The ecosystem and what goes on in an edge data center?

- In understanding what goes on in an edge center, we will look at the bigger picture of the ecosystem of a network architecture, which is broken down to 4 primary tiers and explained as below (CBInsights, 2019) with a simple visual graphic in Figure :-

- The ecosystem of network architecture from bottom up:-

- Edge Sensors and Chips: The first point of data collection. Different technologies are developed and manufactured for a wide range of use cases complementing Application-Specific Integrated Circuits (ASICs) and Application-Specific Standard Products (ASSPs).

- Edge Devices: Devices can range from smart watches to autonomous vehicles and it provides the first line of offense in processing and storing data. It analyses to an extent.

- Edge Infrastructure: Data center comes in all shapes and sizes. The latest trend is deploying edge data center to offer a point between the edge devices and centralized data center. It has more data processing and storage capacity than edge devices and its advantage over centralized data center would be the low latency.

- Centralized Cloud Data Center: This is the main location to store, analyse, and process large scale datasets. It is not a place to analyse and deliver insights needed in real time. This is the final destination for edge data and be added to historic data.

- One of the key characteristics of an edge center is the locality of its location and closeness to the population. It resides on the outer edges of an IP network, connects to a centralized cloud core in a data center, and can be managed remotely. An edge cloud/aggregate is often formed by a group of edge data centers to share network resources.

- The edge data center is a hub hosting the edge server and works as a connection between two separated networks where devices can request data from one network to another. The concept is to move data such as JavaScript files, images, or HTML closest to the requesting machine in order to reduce the time taken for the resources to load (Siemon Interconnect Soultions, 2019). This allows quick and smooth traffic between the networks due to its close proximity to the requesting machine and its location inside an internet exchange point. Following Figure highlights the function of the Edge Data center as a hub connecting between networks.

The future trends of Edge Data Center:-

- The changing economy and our way of life drives the growth for edge computing as we live in a data-driven world. The wave of technologies, from Artificial Intelligence & Machine Learning (AI/ML) to Internet of Things (IoT), to 5G and much more, means that data will need to be closest to the point of use, hence the requirement for many more edge data centers.

- These applications are projected to expand and at the current market, less than 10% of enterprise-generated datasets are processed at the edge, a small number compared to 2025’s 75%, projected exponential growth by van der Meulen, 2018 of Gartner Research.

- Factors driving need for Edge Data Center:

- Arrival of 5G

- Internet of Things (IoT) is growing

- Widening data gap

- Adoption of Software-defined Networking (SDN) and Network-function virtualisation (NFV) tech

- Video streaming and AR/VR

- While expanding rapidly, edge computing is still in its infancy and it will take time but the surge in demand for Edge Data Center will be real. It is projected to accelerate its growth from 2022 onwards where by then, 5G will be fully deployed globally, a key underlying catalyst. Now is the time to get ready for the edge and it is clear at this point, those that invest in edge data centers today will achieve a competitive edge for the future. A new game is developing, and we will have to adapt to the new reality.

- The number of Internet users and subscribers are rising globally and this indicates a positivity towards the growth of Edge Computing and Edge Data Center. The main factors contributing to the growth are: improved device capabilities, increased in data-intensive content, and more affordable data plans. This, coupled with Edge Computing will project a surge globally from 2022 onwards in parallel with the stability of 5G networks.

- Global mobile data traffic per smartphone (GB per month) (ericsson.com, 2019):-

- In the context of developing countries, the understanding and adoption of edge computing is still fairly low. This is reflected in business strategies, deploying Edge Data Centers mainly as a backup infrastructure or part of recovery initiatives. However, Edge has a potential to become more than just a digital trend across the developing nation due to the positive outlook many businesses have in regards to this technology.

- The sizeable and growing population of developing countries and steadily expanding economy as well as increasing technological adoption present many unique growth opportunities. The trade tension between USA and China propels global companies to look elsewhere as they want to reduce their dependence on China and move their operations to other countries. The Edge Data Center market is fairly clear for developing countries – edge technology is the platform of choice and the future is all about adoption, penetration, and applications. The opportunities on the other end are promising and lucrative, just a matter of aligning in the right direction.

EdTech: The new growth catalyst of Indian education industry:-

- The Education industry in India has witnessed maximum disruption during the pandemic. Education today is no longer restricted to just traditional classrooms. The restrictions imposed by the Government and the rigid safety protocols have paved the way to new-age pedagogies.

- A fruitful outcome of these disruptions, however, has been the openness of all stakeholders- the government, private and public schools, tutors, coaching institutes, students, and teachers- in adopting the digital mode of learning, leading to the EdTech boom we are seeing today.

- The Indian EdTech industry is believed to have received a $16.1B in VC funding, a 32X increase from 500M received in 2010. The growth spurt in this industry is driven largely by K-12 Segment, higher education, and upskilling categories.

- Coupled with the growing popularity of Massive Open Online Courses (MOOCs) and distant education India’s EdTech industry is poised to reach $30 billion in the next 10 years. While the long-term impact of the pandemic on the education industry is yet to unfold, learning models are definitely going to go hybrid with smartphone and internet penetration increasing.

- EdTech has the power to bridge the learning gap given technology’s ability to obliterate geographical barriers. As much as educators understand that digital adoption is the need of the hour, they also want to retain a few unparalleled benefits of a traditional classroom setup such as peer discussion, one-on-one support from educators and creating opportunities to work on group collaborative assignments.

- A few of the newer provisions of EdTech include video-assisted remote learning, immersive learning, AI and VR, on-demand learning, etc. However, realising this smoothly would mean that both educators and learners need adequate training to use platform tools for ease of knowledge delivery. As learning demands increase, further technological advancements will progressively be integrated into the classrooms.

- Virtual classrooms can improve student to tutor engagement - Online education is far more affordable in comparison to traditional education (school, college). As per industry reports, education from grade 1 to 12 has increased 6.3 times in 2022 from the base of 2019. Students belonging to different income categories and social classes have been able to access quality education through these platforms because of their affordability, accessibility, and flexibility. Moreover, as online class sizes are smaller than conventional classroom sizes, there is greater time for interactions and feedback between the tutor and the student.

- Adopting artificial intelligence (AI) also offers major educational benefits, such as learning that is customized to each student’s needs, allowing them to adjust the speed and control iterations to enhance the subject’s expertise.

- EdTech platforms that are powered by AI search engines can make things simple. Learners would probably need to fill out a questionnaire at the start. This will help the AI-powered platform to understand the learner’s potential, interests, career options, budget, location, among others. AI is making long strides in the academic world, turning the traditional methods of imparting knowledge into a comprehensive system of learning with the use of simulation and augmented reality tools.

- Government Digital Initiatives will accelerate e-learning adoption - One of the major factors proving impetus to EdTech companies has been the encouraging initiatives from the Indian Government making education accessible to anyone, anywhere. The encouragement and provisions made by the Govt. through initiatives like the SWAYAM (study webs of active learning for young aspiring minds) Diksha, e-pathshala, etc. to encourage educational institutes even in rural towns to switch to online methods of teaching has helped ensure continuity in academic sessions.

- A purpose-built “phy-gital” (physical + digital) platform for educators and learners to come together online. It is the platform wherein , that takes into consideration device and bandwidth issues that are prevalent in the rural as well as semi rural environment and seeks to resolve them for the benefit of students, teachers and institutions.

- Platforms that focus on learning outcomes will thrive - While the potential to scale online learning is immense, weak digital infrastructure has been one of the primary challenges in India for scaling up the active use of technology in education.

- As per reports, only 8 percent-10 percent of Indian households have both a computer and an internet connection. However, the rapid use of mobile phones has believed to boost accessibility and the learning capabilities of students. However, even as accessibility gets addressed, affordability is still a matter of concern when it comes to specialised EdTech products, specifically for lower and lower-middle-income households, limiting its reach.

India's Digital revolution - An opportunity :-

- The Digital Revolution in India started with the Government of India initiating the Digital India programme in July 2015 to transform India into a digitally enabled knowledge-based economy. According to Prime Minister Mr. Narendra Modi, the Digital India programme was developed to better the lives of average citizens. It aimed to make technology "accessible, affordable, and useful" to the country's citizens.

- The effort was divided into different parts: digital infrastructure as a utility for all citizens, governance, on-demand services, and citizen digital empowerment. After six years of this effort, the country has built a strong foundation of digital infrastructure and expanded internet access throughout its economy.

- India is poised for the next phase of growth — the creation of tremendous economic value and the empowerment of millions of Indians as new digital applications permeate and transform a multitude of activities and types of work at a national scale.

- In the last six years, the government has leveraged its digital ecosystem to improve the lives of its citizens. India has used its JAM ecosystem to transfer a total of Rs. 22 lakh crore (US$ 300 billion) through Direct Benefit Transfer (DBT) schemes. The government has also revolutionised the digital payment system.

Critical Drivers for India's Digital Revolution:-

- India has become the world's second-fastest-growing digital economy. The key drivers towards the rapid rise in India's digital ecosystem include:

- Growing Internet Penetration: India's cost per GB of data consumed is the lowest globally, with an average cost of Rs. 50 (US$ 0.7) per GB, India also has the highest data consumption in the world, with an average per-user consumption of 14.1 GB.

- Demographic Dividend: India has the youngest population globally, with an average age of 29; more than 68% of Indians are below the age of 40, out of which 70% of users are already on the internet. India's middle class is expected to comprise a billion people by 2030, 70% of India's population.

- Increasing Smartphone Penetration: According to a study conducted by Deloitte, India is expected to have about 1 billion smartphone users by 2026. India currently has about 750 million smartphone users, and the country is expected to be the second-largest smartphone manufacturer in the next five years.

- India's Robust IT sector: India's IT sector is expected to grow at twice the rate of the economy at 15.5%, and the revenue of the industry is expected to be at US$ 227 billion in 2021-22.

- India has the world's third-largest startup ecosystem, with over 60,000 startups. The country was home to over 94 unicorns in 2021, with a total valuation of US$ 319.67 billion.

- One out of every 13 unicorns globally are born in India. The country witnessed a 60% rise in early-stage capital from 2015 to 2020. India's technology sector witnessed 217 deals worth US$ 14.3 billion in 2021.

- The Indian SaaS ecosystem experienced a 170% increase in investments in 2021, which reached US$ 4.5 billion. More than 35 Indian SaaS enterprises had US$ 20 million or more in annual recurring revenue (ARR) in 2021, a sevenfold growth in five years, with seven to nine of these companies exceeding the US$ 100 million ARR mark as compared to one to two companies five years ago.

- The Indian telecom tower industry has grown by 65% in the last seven years. The government is collaborating on 44 telecom infrastructure projects across the country with multinational investors such as Vodafone, Verizon, Telefonica, Nokia (NOK), SoftBank, and Ericsson.

Recent Government Initiatives for India's digital revolution :-

- Since 2015, the government of India has led the charge in digitisation with its "Digital India" initiative to expand e-governance, providing individuals with access to government entities, expanding digital infrastructure across the country and connecting Indians through the Internet.

- A few of the significant reforms that will further enhance India's Digital revolution are:

- Open Network for Digital Commerce (ONDC): India's Open Network for Digital Commerce is described as the next Unified Payments Interface (UPI) moment for Indian E-commerce. According to the government, Open Network for Digital Commerce (ONDC) is expected to digitise the whole value chain, standardise operations, encourage supplier involvement, improve logistical efficiency, and increase customer value. The ONDC platform has received investments of Rs. 157.5 crore (US$ 20.30 million) for the first stage of the project from 17 banks and financial institutions.

- Drive to provide quality internet: The Government of India has made various investments to provide affordable and quality Internet. These investments include the BharatNet Fiber project and Investments in developing 5G and 6G infrastructure. According to a statement by the Union Minister of Commerce and Industry, Consumer Affairs, Food and Public Distribution and Textiles, Mr. Piyush Goyal, India's 5G ecosystem is expected to contribute US$ 450 billion to the Indian economy in the next 15 years.

- Reforms in India's Digital Payments: The government has pushed UPI to be made available on feature phones to serve rural India. NPCI International Payments Ltd (NIPL) has expanded UPI to a global scale, with nations such as the UAE and Nepal actively participating in the UPI ecosystem. This would boost India's digital transformation and benefit the country globally. In the Union Budget for 2022-23, the government has also revealed plans for a Digital Rupee.

- Push towards Data Centers: To further assist India's digital revolution, the Indian government has announced plans to push investments to build Data centres. The country's data centre capacity will increase to 1.3 GW by 2024, a CAGR of 34%. Mumbai and Chennai are expected to account for 68% of the country's capacity by 2024.

Outlook

- India's digital revolution will cause a paradigm shift for India and its economy. With the help of public and private partnerships, favourable government policies, innovative reforms, demographic advantage, rising incomes and the rise of India's startup culture, India can become the fastest-growing digital economy. India's digital revolution is expected to be a US$ 1 trillion opportunity. The digital revolution has already helped the Indian economy to become resilient to the changing time. In the future, India's digital economy is expected to support India achieve its goal of a US$ 5 trillion economy.

.

No comments:

Post a Comment